At the IFCN webinar “Megatrends in the dairy sector“, held on 6 November 2025, the International Farm Comparison Network reported that milk production has by now crossed the 1bn ton level for the first time. 60% of the milk produced is delivered to processors. From the one million dairy farms worldwide, 3% produce 60% of all milk. The growth rate of milk production used to be around 2.6% p.a. before Corona and has now slowed down to 1.9%. But the „decline“ has hit the formal sector (= milk processed) harder than the informal sector.

Demand, IFCN said, is there and will be there, the question in recent months has been affordability. High product prices have made affordability collapse in a way. Price elasticity is picking in and demand slows, according to IFCN. Record butter prices have opened the door for US imports to Europe, until July 2025 the US have exported 176,000 tons more butter than in the same period of 2024 [not all of this was sold to Europe].

Demand, IFCN said, is there and will be there, the question in recent months has been affordability. High product prices have made affordability collapse in a way. Price elasticity is picking in and demand slows, according to IFCN. Record butter prices have opened the door for US imports to Europe, until July 2025 the US have exported 176,000 tons more butter than in the same period of 2024 [not all of this was sold to Europe].

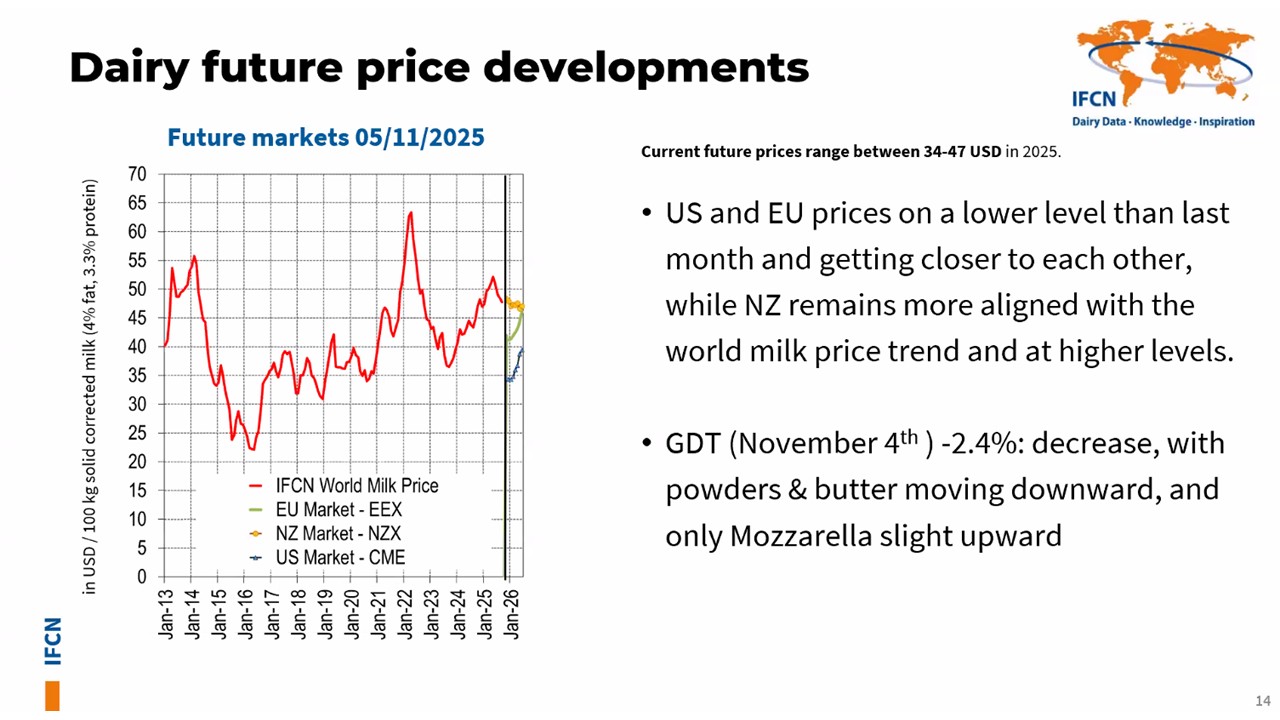

IFCN said that we will see a milk price recovery, given various indexes like dairy futures at EEX into January which point out to the market expectations. But 2026 as whole will see a very tight market situation with China being a typical [dairy] deflation market. And milk fat supply will remain tight.