Global dairy trade continues to grow at a steady pace of around 2% per year, but the underlying dynamics are shifting, according to a new report and the World Dairy Map from RaboResearch. Europe remains the leading exporter but is gradually losing share to the Americas, while weakening Chinese demand is redirecting trade flows toward other emerging markets. At the same time, cheese is powering growth across product categories, and the US and Argentina are increasingly positioned to drive future supply.

Trade growth continues as global flows rebalance

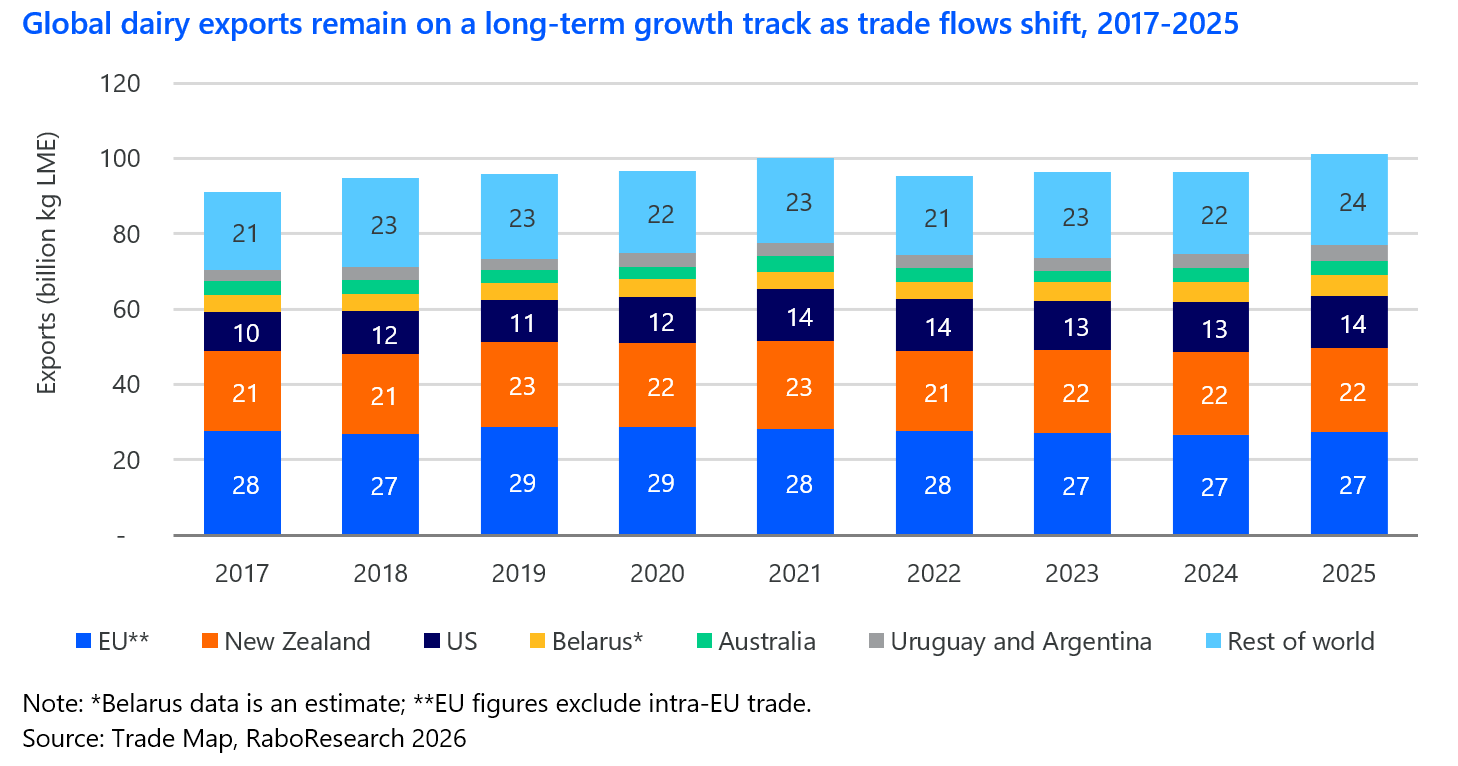

Global dairy trade has maintained its long-term growth trajectory, expanding at an average rate of roughly 2% per year over recent years. Volumes reached more than 100 billion kg in liquid milk equivalents in 2025 – up from 91.1 billion in 2017 –reflecting steady structural demand growth.

Global dairy trade has maintained its long-term growth trajectory, expanding at an average rate of roughly 2% per year over recent years. Volumes reached more than 100 billion kg in liquid milk equivalents in 2025 – up from 91.1 billion in 2017 –reflecting steady structural demand growth.

However, the composition of that growth is changing. The EU remains the largest exporter, accounting for around 27% of global trade, but its share has gradually declined from close to 30% in 2017. Meanwhile, exporters in the Americas are steadily gaining ground, particularly the US, Argentina, and Uruguay.

“Global dairy trade continues to expand at a resilient pace, but the balance of power is shifting,” says Tom Booijink, Senior Dairy Specialist at RaboResearch. “We are seeing a gradual redistribution of export share away from Europe toward more competitive and less constrained producers in the Americas.”

China remains the world’s largest importer, but its role is evolving. Imports have declined significantly from their 2021 peak, driven by increasing domestic production and softer demand in key product categories. “Exporters are increasingly looking to alternative growth markets, including Southeast Asia, the Middle East, and Brazil,” adds Booijink.

Cheese dominates growth, while whey gains strategic value

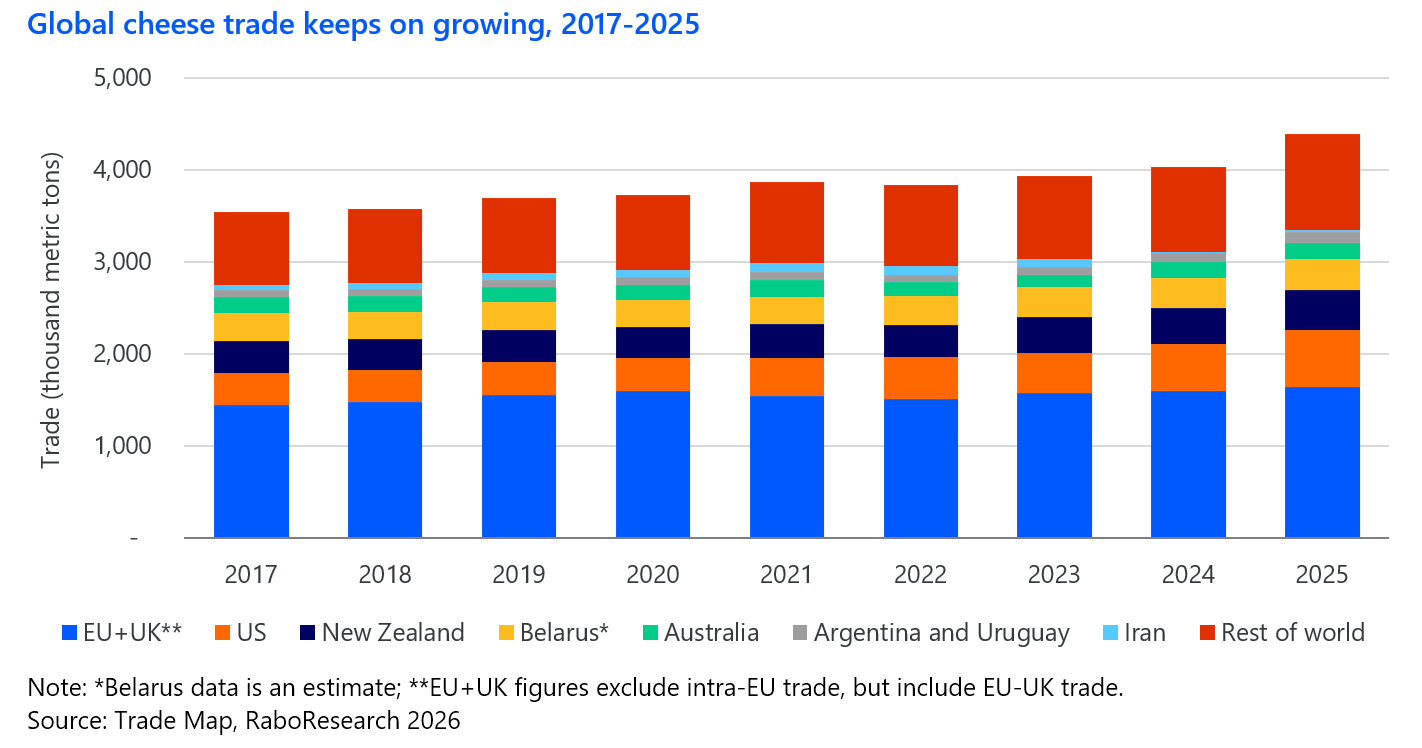

Performance across dairy product categories varies widely, with cheese clearly standing out as the main engine of trade growth. Global cheese trade has increased by roughly 40% since 2017, supported by consistent demand as well as strategic investment in processing capacity.

Performance across dairy product categories varies widely, with cheese clearly standing out as the main engine of trade growth. Global cheese trade has increased by roughly 40% since 2017, supported by consistent demand as well as strategic investment in processing capacity.

“Cheese has become the undisputed growth driver of global dairy trade,” notes Booijink. “Its strong value proposition is encouraging processors worldwide to channel more milk into cheese production.”

At the same time, whey is gaining importance – not in volume, but in value. Rising demand for protein, driven by sports nutrition, health trends, and the growing use of weight‑loss medications, is pushing up prices and increasing its strategic relevance for the industry.

Other segments show more mixed dynamics. Butter trade surged in 2025, driven largely by a sharp increase in US exports, while milk powder markets remain relatively subdued, reflecting slower demand growth and changing export shares among key suppliers.

The US and Argentina to lead future growth

“Global dairy trade is expected to continue expanding along its long-term trend of around 2% annually,” says Booijink. “The key question is which regions will be able to supply that growth.”

Europe’s production is increasingly constrained by regulatory pressures, sustainability considerations, and structural challenges such as an aging farmer population. As a result, its ability to expand output is expected to remain limited.

“The future of dairy trade growth increasingly depends on who can deliver additional milk,” Booijink said. “At this stage, the US and Argentina stand out as the most capable and competitive regions to meet rising global demand.”

Strong investment in processing capacity – particularly in cheese – combined with favorable production conditions is reinforcing the role of these countries in shaping future trade flows.